The Power of Compounding

How compounding works as the engine of long-term wealth, and why not interrupting it matters more than picking the right stocks.

Compounding is the single most powerful force in long-term wealth creation. It is not a strategy — it is a mathematical inevitability that rewards patience and punishes interference.

How Compounding Works

When returns generate further returns, wealth grows exponentially rather than linearly. A 10% annual return does not simply add 10% of the original amount each year — it adds 10% of the growing total. Over decades, the gap between linear and exponential growth becomes enormous.

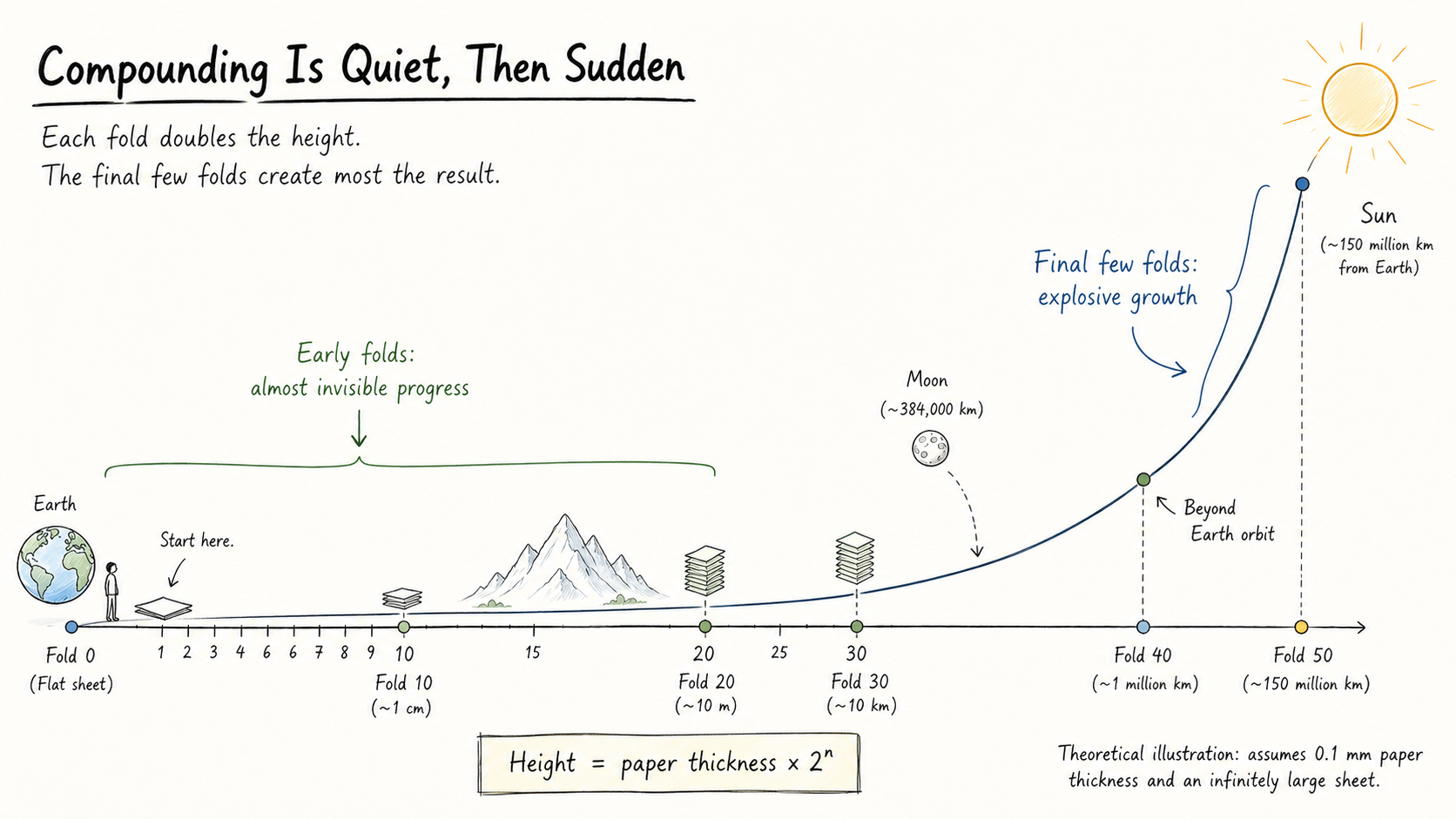

The critical insight is that most of the wealth created by compounding arrives late. The first ten years feel slow. The next ten feel meaningful. The ten after that feel extraordinary. This back-loaded nature is precisely why so few investors capture it — they quit during the slow early phase.

Every exit resets the compounding clock. Selling a position, paying taxes on the gains, and reinvesting the remainder means starting the exponential curve over from a lower base. The cost is not just the transaction fee or the tax — it is the lost trajectory of the curve you abandoned.

Discipline Over Selection

The discipline of not interrupting compounding is more important than picking the right stocks. A mediocre investment held for thirty years will often outperform a brilliant investment held for three. This is counterintuitive because stock selection feels active and skilful, while holding feels passive and lazy. But the mathematics are clear.

The investor who buys a reasonable portfolio and never touches it will, over a long horizon, outperform most investors who trade frequently — not because of superior insight, but because of inferior interference.

Compounding works on habits too. The discipline required to leave investments alone is itself a skill that compounds. Each year of patience makes the next year easier. Each resisted urge to tinker strengthens the habit of restraint. Over time, the investor who compounds discipline has a structural advantage that no amount of clever trading can replicate.

The Enemy of Compounding

The greatest threat to compounding is not market crashes or recessions — it is the investor's own behaviour. The urge to act, to respond, to optimise. Every unnecessary transaction is a leak in the compounding vessel. Taxes, fees, and the inevitable mis-timing of re-entry all erode the curve.

The best thing most investors can do is recognise that compounding requires almost nothing from them except the willingness to do almost nothing.

Related

- The Long-Term Mindset — why doing nothing is consistently the correct response

- Quality Investing — holding excellent businesses through the full compounding journey

- Equity Risk Premium — the return that compounds when you simply stay invested