The Long-Term Mindset

Why equities are the best-performing asset class over long horizons, and why the most powerful strategy is also the simplest: buy consistently, hold patiently, do almost nothing.

Long-term investing is not just a financial strategy — it is a calmer way to live. When you are not monitoring every tick, volatility becomes background noise rather than a source of anxiety. The daily movements of the market lose their urgency. Most developments, on inspection, require no response at all.

Equities as the Dominant Asset Class

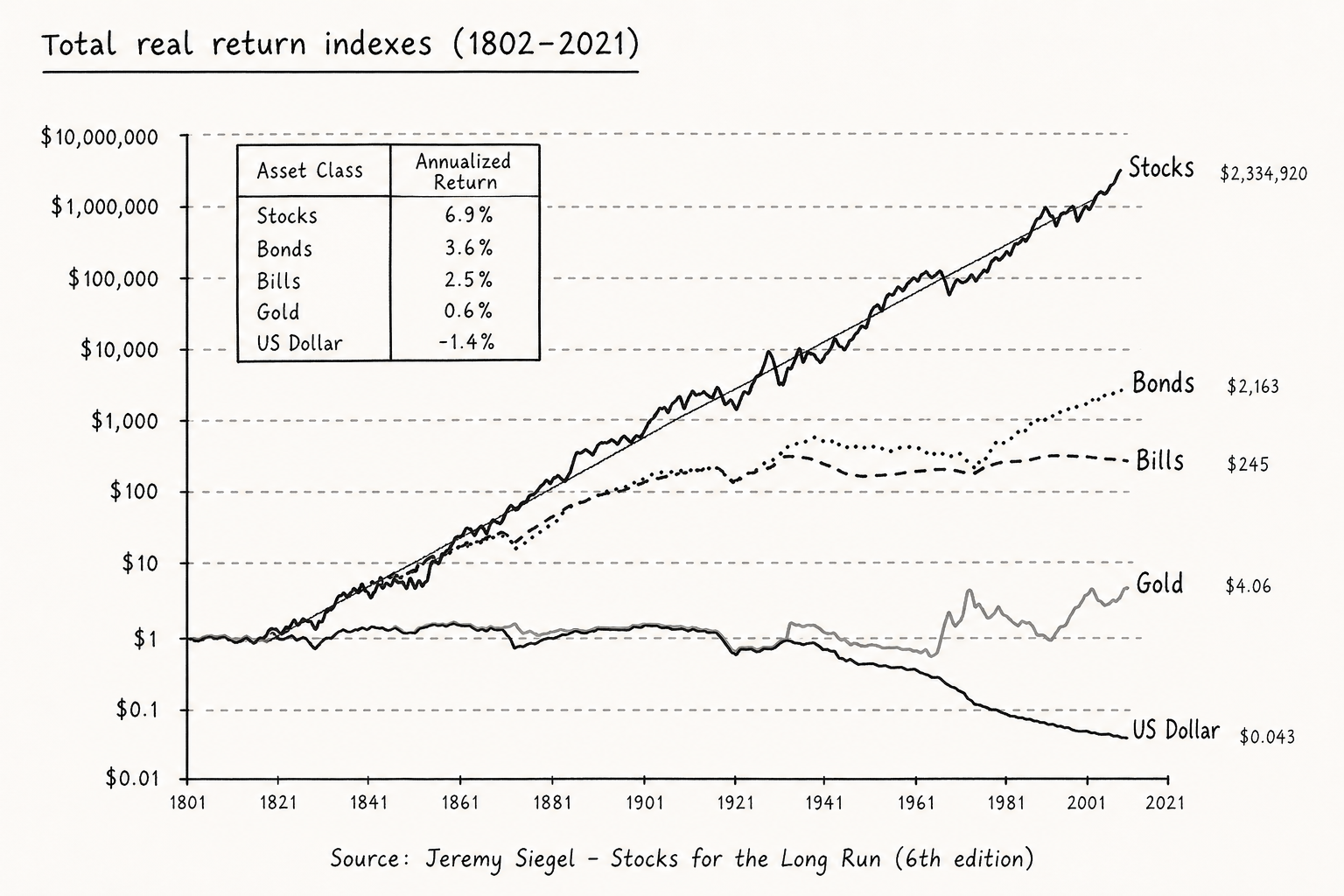

Over the past two centuries, equities have dramatically outperformed every other major asset class. Jeremy Siegel's data on total real return indexes from 1802 to 2021 makes the case unambiguously:

- Stocks: 6.9% annualised real return — $1 invested in 1802 grew to $2,334,920

- Bonds: 3.6% annualised real return — growing to $2,061

- Bills: 2.5% — growing to $245

- Gold: 0.6% — growing to $4.52

- US Dollar: lost value in real terms over the same period

The gap between stocks and every other asset class is not marginal — it is orders of magnitude. This is the single most important chart in investing. It tells you that over a long enough horizon, the question is not whether to own equities, but how much.

The outperformance is not an accident. Equities represent ownership of businesses that innovate, adapt, and generate surplus value. Bonds are contractual claims with capped upside. Gold produces no cash flow. Cash erodes with inflation. Only equities compound human productivity into wealth.

Time to Compound

The catch is that equities need time. Over any single year, stocks can lose 30% or more. Over five years, the range of outcomes is still wide. But over twenty years, stocks have almost never delivered a negative real return. The longer you hold, the more reliably equities deliver their structural advantage.

This is why the long-term mindset matters so much. The asset class itself does the work — but only if you give it time. Every exit, every pause, every rotation into cash interrupts the compounding engine. The investor who stays invested for thirty years captures the full curve. The one who dips in and out captures fragments.

The Value of Inaction

Very few developments in financial markets require a response from a long-term investor. Recognising this — and doing nothing — is consistently the correct decision.

The enemy of good returns is not ignorance but activity. Every unnecessary transaction carries direct costs (fees, taxes, spreads) and indirect costs (resetting the compounding clock, mis-timing re-entry, emotional depletion). The cumulative drag of frequent activity is enormous over a multi-decade horizon.

The financial industry is structured to encourage action. News, alerts, analyst ratings, earnings surprises — all of it is designed to make you feel that something must be done. The long-term investor's most valuable skill is the ability to receive all of this information and conclude, correctly, that no action is required.

Simplicity as Strategy

The most powerful investment strategy is also the simplest:

- Buy consistently — regular contributions regardless of market conditions

- Hold patiently — through drawdowns, corrections, and bear markets

- Do almost nothing — resist the urge to optimise, tinker, or respond

This is not laziness. It is discipline. Doing nothing in the face of constant provocation to act requires more conviction than trading does.

In most domains, more effort produces better results. In investing, the relationship is often inverted. The investor who spends ten hours a week analysing markets and adjusting positions will frequently underperform the investor who spends ten minutes a month contributing to an index fund. This is uncomfortable because it suggests that much of what passes for investment skill is actually value-destroying activity.

What This Looks Like in Practice

A long-term investor's year might look like this:

- Twelve monthly contributions to a portfolio

- One or two reviews of holdings to confirm business quality remains intact

- Zero trades in response to news, earnings, or market movements

- Perhaps one rebalancing event if allocations have drifted significantly

That is not inattention. It is the correct level of attention for the chosen time horizon.

Related

- The Power of Compounding — what happens when you leave investments alone long enough

- Handling Volatility — why short-term pain smooths out over long horizons

- Time Horizon as Analytical Constraint — matching your behaviour to your actual timeframe

- Equity Risk Premium — the return you earn by enduring volatility instead of fleeing it