Time Horizon as Analytical Constraint

How the timeframe you choose determines the tools that matter — and why most investors misjudge their own horizon until a drawdown tests it.

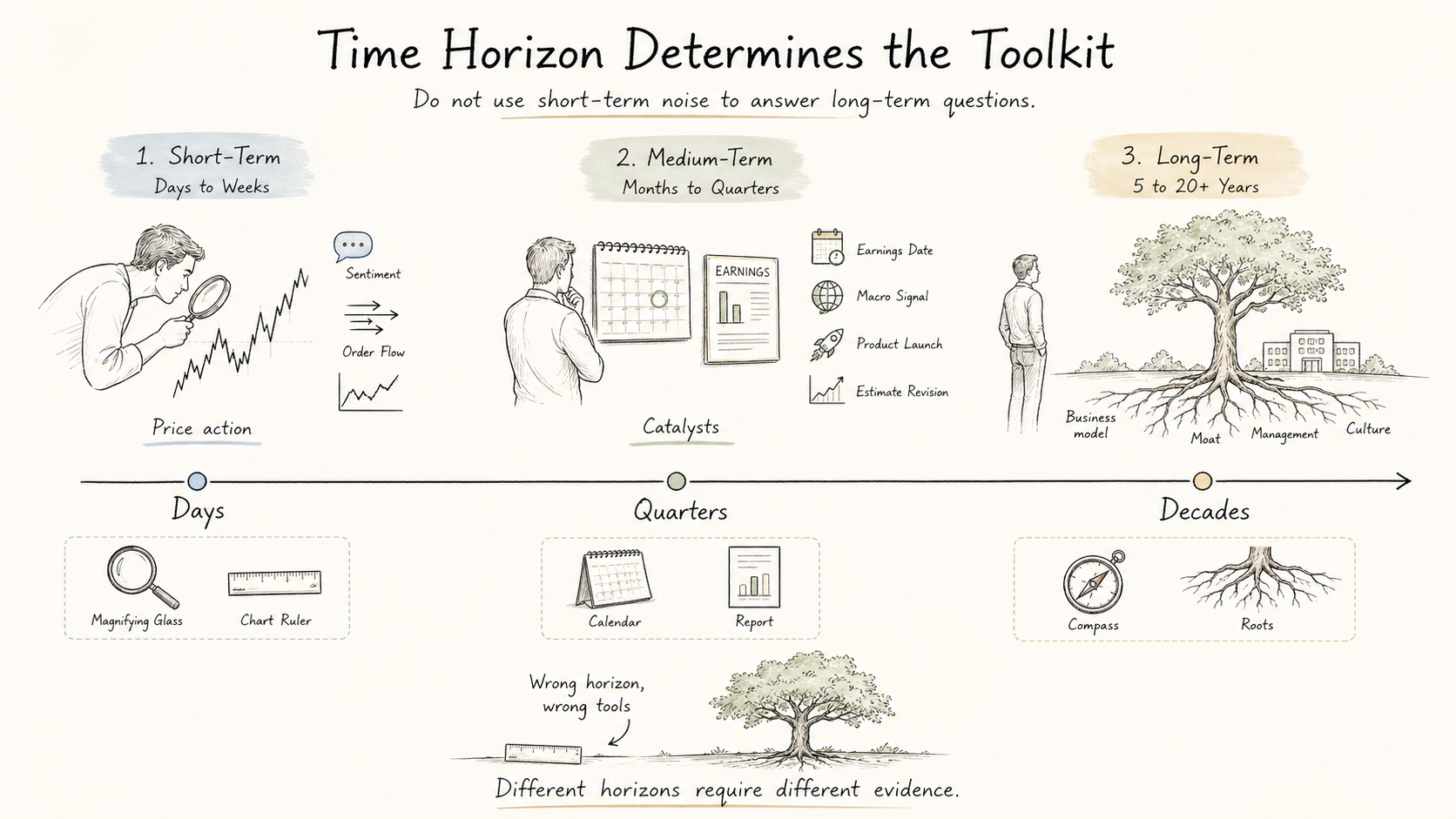

Time horizon is not a preference — it is an analytical constraint. The timeframe you operate within determines which information matters, which tools are appropriate, and which risks are real. Using the wrong toolkit for your horizon is one of the most common and costly mistakes in investing.

Three Distinct Timeframes

Short-Term (Days to Weeks)

The relevant toolkit includes technical analysis, chart patterns, sentiment indicators, and order flow. Price action dominates. Fundamentals are nearly irrelevant at this scale because they do not change day to day. The edge, if any exists, comes from reading the behaviour of other market participants.

Medium-Term (Months to Quarters)

Catalysts drive returns at this scale: earnings releases, macro shifts, regulatory changes, product launches. The toolkit expands to include fundamental analysis, but focused on near-term changes rather than durable characteristics. Analysts' estimates and revisions matter. Positioning and expectations matter.

Long-Term (5 to 20+ Years)

The relevant toolkit is entirely different. What matters is:

- Business model stability — will the way this company makes money still work in a decade?

- Competitive moats — are the barriers to competition durable or eroding?

- Management philosophy — does leadership think in years or quarters?

- Culture — is the organisation built to adapt and endure?

Culture, moats, and business model logic are stable across economic cycles in ways that quarterly earnings, margins, and revenue growth rates are not. A company's Q3 earnings miss tells you almost nothing about its position in 2036. Its competitive structure and organisational culture tell you a great deal.

The Honest Difficulty

Most investors claim a long-term horizon. Very few actually have one. The test is not what you say during a bull market — it is what you do during a 30% drawdown.

Your actual time horizon is revealed during drawdowns, not during calm markets. If a 20% decline causes you to sell, your horizon was never long-term regardless of what you told yourself. Knowing your real horizon — and being honest about it — is a prerequisite for choosing the right analytical framework.

The structural problem is that long-term investing requires ignoring most of the information the financial industry produces. Quarterly earnings, daily price movements, analyst upgrades and downgrades — almost none of this matters on a 10-year horizon. But it is loud, constant, and designed to provoke action. The long-term investor must build a filter that excludes most of what the market considers important.

Matching Horizon to Method

Mismatched horizons and methods destroy returns. Common errors include:

- Using technical analysis to make long-term allocation decisions

- Using long-term fundamental analysis to time short-term trades

- Buying a stock for its decade-long potential, then selling it after a bad quarter

- Claiming to be a long-term investor while checking portfolio value daily

The discipline is not just choosing a horizon — it is committing to the toolkit that matches it, and ignoring everything else.

Related

- The Long-Term Mindset — the psychological discipline required to operate on a long horizon

- Quality Investing — the approach built for the long-term timeframe

- The Power of Compounding — why long horizons unlock exponential growth