Equity Risk Premium

The excess return that equities deliver over risk-free assets, and why capturing it requires no special skill — only the willingness to stay invested.

The equity risk premium (ERP) is the excess return that equities deliver over risk-free assets such as government bonds. Historically, this premium has averaged roughly 4% per year. It is the foundational reason why long-horizon investors allocate to equities.

Why the Premium Exists

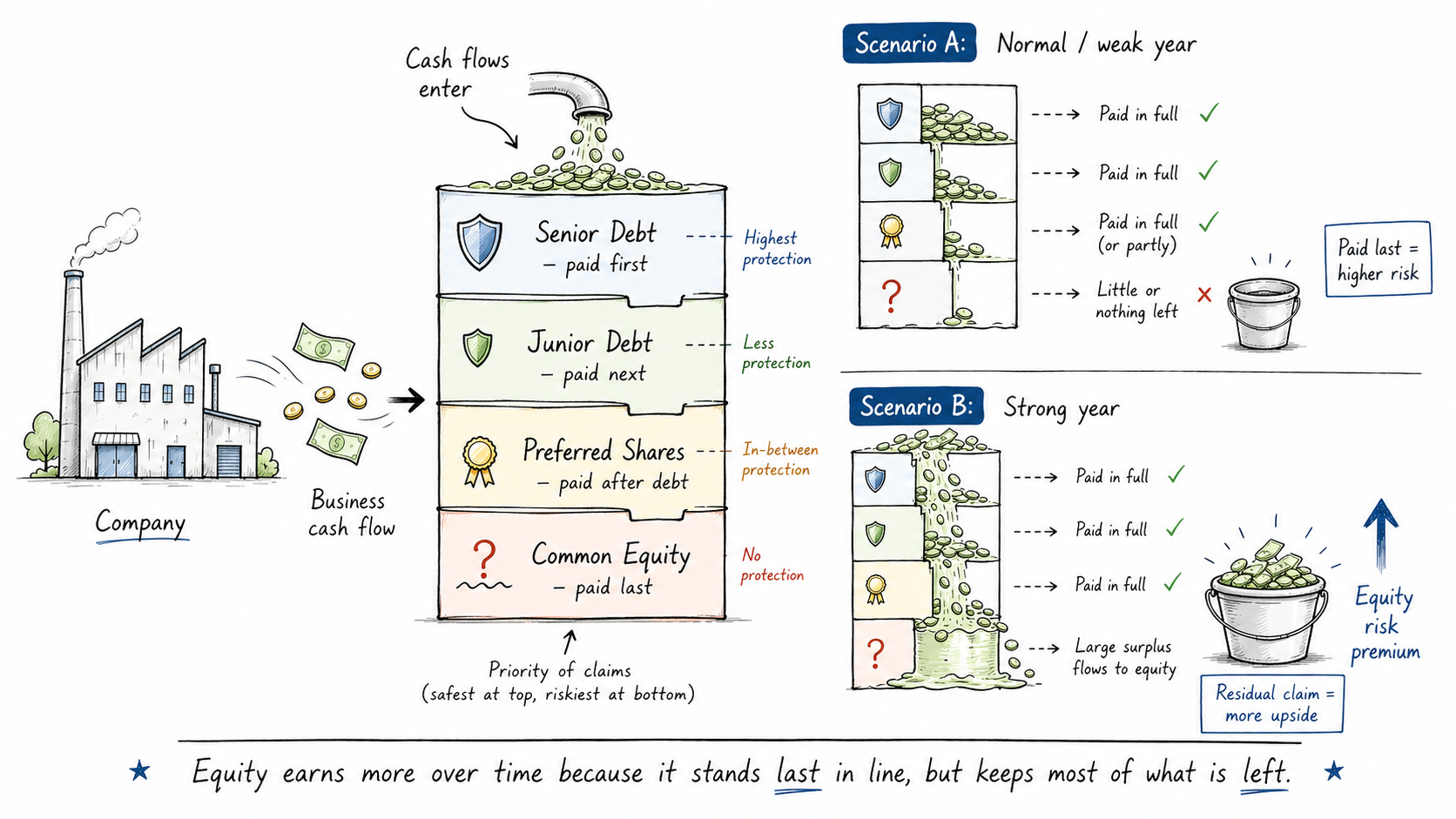

Equity holders are residual claimants on a business. After employees, suppliers, lenders, and tax authorities have been paid, whatever remains belongs to shareholders. This means equity holders bear the most risk — but they also capture all the upside.

Bondholders receive fixed coupons. Their return is capped by contract. Equity holders have no such ceiling. When a business grows its earnings, bondholders receive exactly what they were promised. Equity holders receive everything above that.

The equity risk premium is not an empirical accident. It follows from the structure of corporate claims. As long as businesses generate surplus value above their fixed obligations, equity holders will earn more than bondholders over time. This is a structural argument, not a historical pattern that might vanish.

Think of a company's cash flows as water poured into a stack of buckets. Senior debt gets filled first — reliable, but capped. Junior debt next. Preferred shares after that. Common equity sits at the very bottom, the last bucket to receive anything. In a weak year, equity holders may get little or nothing. But in a strong year, every bucket above is already full, and the overflow pours entirely into equity. The premium exists because equity earns more over time precisely by standing last in line but keeping most of what is left.

Capturing the Premium

The most important insight about the equity risk premium is that you do not need stock-picking skill to capture it. Simply staying invested in a broad equity index is sufficient.

Passive participation in the S&P 500, MSCI ACWI, or any diversified equity index captures the premium. The premium belongs to anyone willing to bear equity risk over a long horizon. It does not require:

- Timing the market

- Selecting individual stocks

- Following macro forecasts

- Monitoring daily price movements

It requires only one thing: staying invested.

Every period spent out of equities is a period where the risk premium is forfeited. Cash and bonds are not neutral — they carry an opportunity cost equal to the equity risk premium. For long-horizon investors, the question is not whether equities are risky in the short term, but whether the premium compensates for that risk over the full horizon. Historically, for periods longer than ten years, the answer has been overwhelmingly yes.

Implications for Portfolio Construction

If the equity risk premium is structural and capturable through passive investment, then the primary job of a long-term investor is not security selection — it is remaining invested through volatility. The premium is the reward for enduring drawdowns without exiting. Those who sell during downturns forfeit the very compensation they were being paid to bear.

Related

- The Power of Compounding — the equity risk premium is what compounds when you stay invested

- Time Horizon as Analytical Constraint — why the premium only reliably appears over long horizons

- The Long-Term Mindset — the psychological framework for capturing the premium